Understanding Charges and Rates on Equity Release Mortgages

Understanding Charges and Rates on Equity Release Mortgages

Blog Article

Just How Equity Release Mortgages Can Impact Your Financial Future and Retirement Plans

Equity Release home loans present both possibilities and obstacles for individuals planning their monetary futures and retired life. They can give prompt liquidity, alleviating the worry of living costs. However, these items also diminish the worth of estates, affecting inheritance for successors. Comprehending the subtleties of equity Release is crucial. As individuals discover their choices, they must think about the wider effects on their monetary wellness and heritage. What choices will they encounter in this complicated landscape?

Understanding Equity Release Mortgages: What You Required to Know

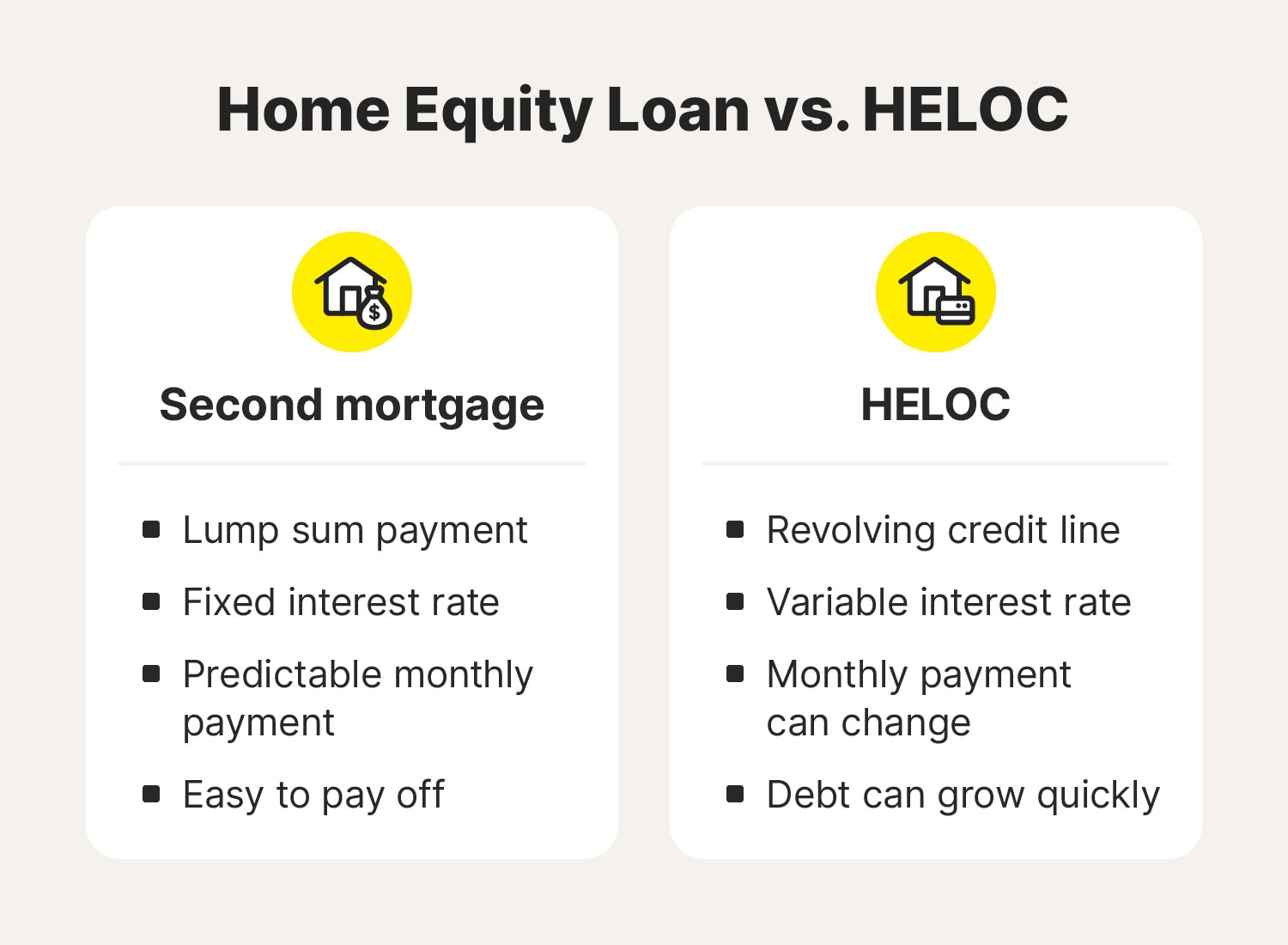

:max_bytes(150000):strip_icc()/dotdash_Final_Home_Equity_Loan_vs_HELOC_What_the_Difference_Apr_2020-01-af4e07d43f454096b1fbad8cfe448115.jpg)

Kinds Of Equity Release Products Available

Equity Release products come in different kinds, satisfying various demands and choices of home owners. Both main types are life time mortgages and home reversion plans.Lifetime home mortgages enable homeowners to obtain versus their residential or commercial property while keeping ownership. The lending, plus interest, is commonly repaid upon fatality or when the home is offered. This option provides adaptability and permits continued house in the home.Conversely, home reversion prepares involve offering a part of the residential property to a company for a lump sum or normal payments. The home owner maintains the right to live in the home until they pass away, but the company gains possession of the offered share.Both items have unique advantages and factors to consider, making it essential for individuals to evaluate their economic situations and lasting goals prior to proceeding. Recognizing these choices is necessary for notified decision-making relating to equity Release.

How Equity Release Can Give Financial Alleviation in Retired Life

Immediate Cash Accessibility

Several senior citizens encounter the difficulty of taking care of fixed revenues while maneuvering increasing living costs, making prompt money access an important factor to consider. Equity Release home mortgages provide an efficient remedy, enabling property owners to access the value of their properties without the requirement to market. This economic system makes it possible for retirees to access a lump sum or routine settlements, offering them with the essential funds for day-to-day expenditures, unexpected expenses, or also leisure activities. By tapping right into their home equity, retired people can alleviate financial stress and anxiety, preserve a comfy lifestyle, and preserve their financial savings for emergencies. Immediate money accessibility via equity Release not only boosts monetary flexibility however additionally empowers retired people to enjoy their retired life years with higher assurance, totally free from instant monetary constraints.

Financial Obligation Consolidation Benefits

Accessing immediate money can substantially improve a retired person's financial situation, however it can likewise offer as a strategic device for managing current debts. Equity Release home loans offer a possibility for retired people to use their home equity, supplying funds that can be made use of to settle high-interest financial debts. By paying off these debts, retirees might lower regular monthly financial burdens, permitting an extra workable spending plan. This approach not just streamlines finances but can likewise enhance general economic security. Additionally, the cash money acquired can be designated toward essential expenses or financial investments, further supporting retirement. Inevitably, making use of equity Release for debt loan consolidation can bring about considerable lasting economic alleviation, allowing retired people to appreciate their golden years with greater comfort.

The Impact of Equity Release on Inheritance and Estate Planning

The decision to utilize equity Release can substantially change the landscape of inheritance and estate preparation for people and their family members. By accessing a part of their home's value, property owners may significantly reduce the equity readily available to pass on to heirs. This option can develop an intricate dynamic, as individuals should consider prompt financial needs against lasting heritage goals.Moreover, the funds launched through equity can be used for various functions, such as boosting retirement way of lives or covering unanticipated expenses, however this typically comes at the expenditure of future inheritance. Families might face tough conversations concerning expectations and the ramifications of equity Release on their monetary legacy.Additionally, the responsibilities tied to equity Release, such as payment problems and the capacity for diminishing estate value, need cautious consideration. Ultimately, equity Release can reshape not only monetary scenarios yet additionally household connections and expectations bordering inheritance.

Tax Obligation Effects of Equity Release Mortgages

The tax obligation implications of equity Release home mortgages are essential for house owners considering this option. Especially, resources gains tax and estate tax can substantially impact the economic landscape for people and their heirs (equity release mortgages). Recognizing these factors to consider is important for reliable economic planning and management

Funding Gains Tax Considerations

While equity Release mortgages can give house owners with immediate financial relief, they likewise carry possible tax ramifications that must be meticulously thought about. One vital facet is capital gains tax (CGT) When a house owner releases equity Homepage from their home, they may encounter CGT if the home value boosts and they make a decision to market it in the future. The gain, which is calculated as the distinction between the market price and the initial purchase cost, is subject to tax. Property owners can benefit from the main home relief, which might spare a section of the gain if the property was their major home. Recognizing these subtleties is crucial for house owners preparing their monetary future and examining the long-lasting impact of equity Release.

Estate Tax Effects

Taking into consideration the prospective effects of inheritance tax is crucial for homeowners opting for equity Release mortgages. When property owners Release equity from their building, the amount taken out may affect the value of their estate, potentially boosting their estate tax obligation. In the UK, estates valued over the nil-rate band threshold undergo inheritance tax obligation at 40%. Therefore, if a home owner uses equity Release to money their retirement or other expenses, the staying estate may significantly minimize, affecting recipients. Property owners should think about the timing of equity Release, as very early withdrawals can lead to higher tax obligation ramifications upon death. For this reason, recognizing these factors is important for reliable estate planning and making sure that recipients receive their desired tradition.

Evaluating the Risks and Benefits of Equity Release

Equity Release can use considerable monetary benefits for home owners, yet it is vital to evaluate the affiliated risks prior to continuing. One of the main advantages is the capacity to access tax-free cash, allowing individuals to money their retired life, make home renovations, or assist relative monetarily. The effects on inheritance are considerable, as launching equity reduces the value of the estate passed on to heirs.Additionally, passion prices on equity Release products can be higher than standard mortgages, leading to increased financial debt over time. House owners have to likewise take into consideration the prospective effect on means-tested benefits, as accessing funds may affect eligibility. The intricacy of equity Release products can make it challenging to understand their long-term ramifications fully. Therefore, while equity Release can give instant economic alleviation, a detailed analysis of its benefits and dangers is vital for making knowledgeable decisions regarding one's monetary future

Making Informed Decisions About Your Financial Future

Home owners encounter a multitude of selections when it concerns handling their monetary futures, particularly after pondering choices like equity Release. Enlightened decision-making is important, as these options can considerably impact retired life strategies and overall monetary health and wellness. Homeowners must begin by thoroughly researching the ramifications of equity Release, including possible effect on inheritance and future care expenses. Involving with monetary advisors can offer customized understandings, making it possible for individuals to recognize the long-term consequences of their decisions.Moreover, home owners need to consider alternate choices, such as downsizing or other kinds why not check here of funding, to determine the most appropriate path. Assessing one's financial scenario, consisting of properties and financial debts, is crucial for making a versatile choice. Inevitably, a cautious evaluation of all offered alternatives will certainly equip home owners to navigate their financial futures confidently, ensuring they straighten with their retirement objectives and individual ambitions.

Frequently Asked Concerns

Can I Still Move Home if I Have an Equity Release Home Loan?

The person can relocate home with an equity Release mortgage, yet need to follow certain lender problems. This usually includes repaying the existing mortgage, which can impact their economic scenario and future plans.

Exactly How Does Equity Release Affect My State Advantages Qualification?

Equity Release can influence state benefits eligibility by boosting assessable earnings or resources. Individuals might experience reductions in advantages such as Pension plan Credit or Real estate Benefit, potentially impacting their overall financial support during retired life.

What Occurs if I Outlive My Equity Release Strategy?

If a specific outlives their equity Release strategy, the home mortgage usually remains basically until their passing away or relocating into long-term care. The estate will be responsible for resolving the financial debt from the residential property's worth.

Can I Repay My Equity Release Home Mortgage Early?

Paying off an equity Release mortgage very early is generally possible however might entail charges or penalties. Borrowers must consult their lender for details terms, as each strategy varies in problems pertaining to very early settlement choices.

Are There Age Restrictions for Requesting Equity Release?

Equity Release normally enforces age restrictions, often requiring candidates to be at the very least 55 or 60 years of ages. These constraints ensure that people are approaching retired life, making the scheme preferable for their economic circumstance.

Final thought

In recap, equity Release home loans Get More Info use a potential economic lifeline for retired people, giving prompt cash money accessibility to boost lifestyle. Nevertheless, they come with considerable factors to consider, including effects on inheritance, estate preparation, and tax obligation liabilities. Thoroughly reviewing the risks and advantages is vital for ensuring that such decisions align with long-lasting monetary goals. Consulting with a financial expert can help individuals browse these intricacies, inevitably supporting a more safe and informed economic future. Equity Release mortgages are financial items created for property owners, typically aged 55 and over, permitting them to access the equity connected up in their residential or commercial property. Equity Release home loans offer a possibility for senior citizens to tap right into their home equity, providing funds that can be used to combine high-interest financial obligations. Households may deal with hard discussions concerning assumptions and the implications of equity Release on their economic legacy.Additionally, the commitments connected to equity Release, such as repayment problems and the potential for lessening estate value, need cautious consideration. While equity Release home mortgages can offer homeowners with immediate monetary alleviation, they also lug prospective tax effects that need to be thoroughly considered. The ramifications on inheritance are considerable, as releasing equity lowers the value of the estate passed on to heirs.Additionally, passion rates on equity Release products can be higher than typical home mortgages, leading to increased financial obligation over time.

Report this page